Andres Mäe

Analyst

EU member states should not be afraid to give up Russian supplies

The main arguments that the leaders of European energy companies, especially in Germany, but also in Austria, Italy and France—and under their influence also local politicians1—have presented in favour of increasing imports of Russian natural gas are that more expensive alternatives (for example, acquiring liquefied natural gas from the Middle East or the US) would undermine the competitive position of European industry2 and that the decline of natural gas production in Europe can only be offset by importing more from Russia.3

Russia, which largely depends on revenue from fossil fuel exports, welcomes this approach, because it allows it to continue the export of its second-biggest product (after oil) at least on the same scale as before its aggression against Ukraine in the spring of 2014.

Although countries often want to claim importing natural from Russia is a purely economic activity, it is not an isolated process that doesn’t affect other fields of international life. Given the dependence of Russia’s national budget on revenue from oil and natural gas exports and taking into account Russia’s military ventures against Georgia and Ukraine, the justifications of European leaders who emphasise the continent’s dependence on Russian natural gas appear surprising, to put it mildly. Russia’s military expenditure is significantly higher than that of European countries.4,5 In 2018, for example, it was 3.9% of GDP or about 2.6 times the average of EU member states. Although Western countries have imposed sanctions on Russia due to its aggression against Ukraine, these do not affect the export of oil and natural gas.

According to the Russian Ministry of Finance,6 exports contributed 30.7% of GDP in 2018. Fossil fuels, in turn, amounted to 63.7% of exports, and natural gas 12.1%. Through mining fees and export taxes, fossil fuels contributed about 46.9% to state revenue in 2018.7 Crude oil exports amounted to 34.9% of the state budget. Consequently, natural gas exports accounted for about 7.4% of Russia’s national budget revenue in 2018 and 3.7% of GDP—the latter figure about the same as defence spending.

In the following section I endeavour to assess how burdensome it would be for EU member states to import natural gas from sources other than Russia, and compare the cost of this process to the economy with the share of GDP accounted for by defence spending.

According to Eurostat data, EU member states consumed 471.7 billion cubic metres (bcm) of natural gas in 2018. The Russian Federation Customs Service8 states that 149.7 bcm of natural gas was exported to EU member states in 2019.

Eurostat’s database provides the prices of natural gas in three groups for households and five groups for business on the basis of annual consumption. The proportions for all price groups are not specified in the database, but they are given for an average group of both consumer categories—D2 for households and I3 for business. In the following analysis, the price before tax for natural gas sold to the average group of companies (annual consumption between 10,000 and 100,000 gigajoules (GJ)) has been extended to all businesses.

Given the significant proportion of business’s natural gas consumption within the EU (at least 65%, and on average 81%, of the total), the following analysis is limited to companies and seeks to assess the impact that changing the source of supply would have on economic competitiveness.

In Figure 1, EU member states are distributed according to companies’ consumption of natural gas as a proportion of the national total and the price they pay.

Sweden and Finland are grouped together as the price of natural gas sold to companies there is substantially higher than in other member states. Unlike Sweden, Finland imports natural gas from Russia. The following calculations and analyses are based on the price of natural gas sold to Swedish companies, which was by far the highest in the EU in 2018, assuming that it corresponds, with the minimum of error, to the price of natural gas delivered from some alternative non-Russian source of supply.

Figure 1. Business share of natural gas consumption (x axis) and the price of natural gas sold to companies (y axis) in EU member states, 2018

Next we compare the ratio of defence spending in EU member states to imports of natural gas from Russia, based on the corresponding shares of GDP.

In calculating the ratio of natural gas imported from Russia, the amount of natural gas consumed in a member state based on Eurostat data (a) was multiplied by the share of natural gas imported from Russia (b), the proportion of total consumption account for by business (c), and the price of natural gas sold in the relevant countries to companies belonging to the average group, I3 (d).

The quantities of natural gas on which the share of imports from Russia is based are taken from the database of the Russian Federation’s Customs Service, in which—unlike the annual accounts of Gazprom or Gazprom Export, for example—only the export of natural gas produced in Russia is reported.

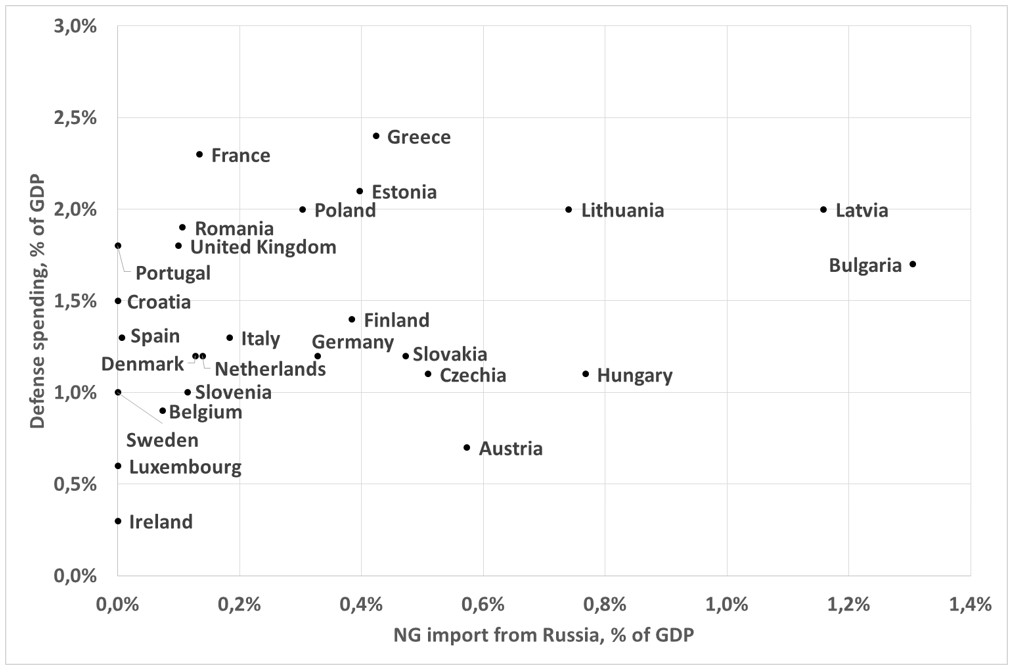

In Figure 2, the distribution of EU member states is based on their defence spending and natural gas imports from Russia as a proportion of GDP. (Bulgaria’s position in the chart can be explained by the country’s relatively modest GDP.) Latvia and Lithuania form a notable group. Given their relatively high defence spending (about 2% of GDP), the proportion of GDP made up by Russian natural gas imports seems somewhat surprising.

Figure 2. Defence expenditure of EU member states (y axis) compared to their spending on natural gas imported from Russia (x axis) as a proportion of GDP, 2018

This allows us to pose the question: what proportion of GDP is a country prepared to allocate to natural gas imported from some other source of supply, rather than lining the pocket of a hostile neighbouring country that ignores international agreements and has launched military aggression at least twice within the last dozen years?

In order to identify the additional costs that would be incurred if natural gas was imported from some other (presumably more costly) source of supply instead of Russia, I replaced the price of natural gas sold to other EU member states with the highest price (the price paid by Swedish companies). Based on the change in the proportion of GDP, I determined the estimated cost to a specified country’s economy of replacing Russian supply.

In Figure 3, the distribution of EU member states is based on their defence spending and the share their economies would lose if they imported natural gas for business at presumably higher prices than gas imported from Russia. Both variables are given as a proportion of GDP.

Figure 3. Additional costs incurred by EU member states upon buying more expensive natural gas, as a proportion of GDP

Again, Bulgaria’s location in the chart may be due to its relatively low GDP. Bulgaria would lose the most of any EU member state—its GDP would be reduced by 0.7% if it did not import natural gas from Russia and local businesses had to pay the same price as Swedish companies.

The loss would be relatively high for Hungary and Latvia too, with GDP decreasing about 0.4% if they imported natural gas from somewhere other than Russia.

The growing dependence of European countries on imports of natural gas from Russia is a point of concern because trade in energy based on unsustainable business models and with an aggressive state poses a potential security risk.

Replacing Russian natural gas with gas imported from some other part of the world would impact EU member states to the extent of reducing their GDP by an average of 0.13%. In other words, the impact would not be so great as to be intolerable for their economies.

Replacing Russia as the source of supply would be a heavier burden for Eastern and Central European countries than for the more prosperous Western European countries (with the exception of Austria). Germany, the Netherlands and Italy might not even notice the difference.

There are alternative sources, especially for the Baltic states, where all the natural gas consumed could be imported through Lithuania’s LNG terminal. Besides, sources can also be replaced in part—for example, by half.

______

1 https://www.err.ee/948932/merkeli-uue-energiapoliitika-osaks-on-ka-nord-stream-2.

2 See, e.g., the opinions voiced in favour of the Nord Stream 2 pipeline construction in Marco Siddi, “Russia’s evolving gas relationship with the European Union”, Energypost.eu, 15 October 2018, https://energypost.eu/russias-gas-relationship-with-europe/.

3 See, e.g., the series of articles by Alex Barnes in The Baltic Course – http://www.baltic-course.com/eng/energy/?doc=141330; http://www.baltic-course.com/eng/energy/?doc=141331; http://www.baltic-course.com/eng/energy/?doc=150197; http://www.baltic-course.com/eng/energy/?doc=141211.

4 Between 2010 and 2015, Russia’s national defence expenditure was between 4.9% and 16% of GDP.

5 All data on defence spending used in this article is derived from the fact sheet “Trends in World Military Expenditure, 2018” by the Stockholm International Peace Research Institute (SIPRI), April 2019, https://www.sipri.org/sites/default/files/2019-04/fs_1904_milex_2018_0.pdf.

7 https://www.minfin.ru/ru/statistics/fedbud/execute/.

This article was published in ICDS Diplomaatia magazine.